During the height of the Covid lockdowns, many people were fortunate enough to be able to save a lot of money. This was in large part down to not being able to spend. However, over the course of the last 12 months, those savings have come under attack by rising inflation.

Although most people associate inflation with higher food and energy costs, inflation also reduces the value of money, and savings over time. Here are some examples of how inflation impacts the real value of money under different situations.

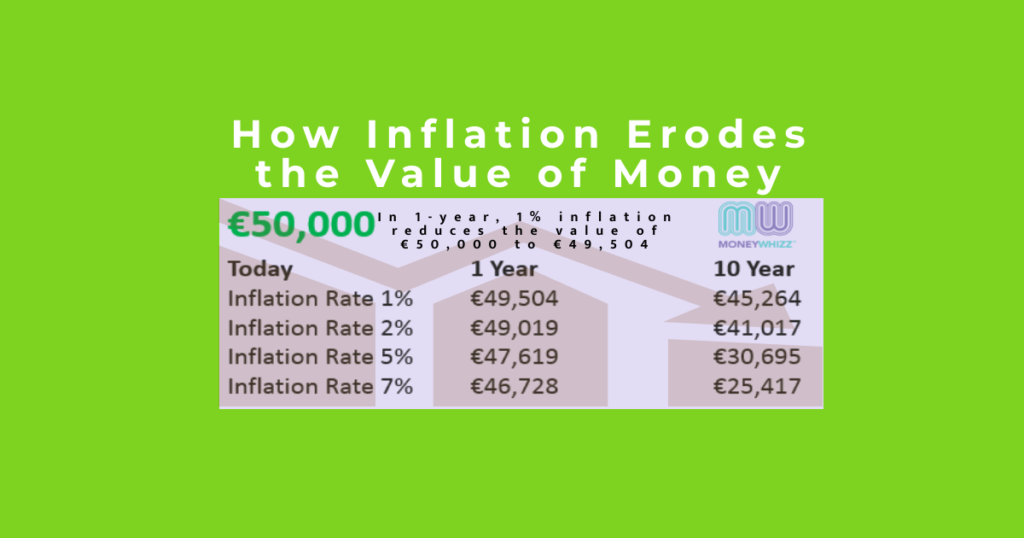

Let’s say we take a saver with €50,000 on deposit. If the rate of inflation is 5%, in just one year, the ‘buying power’ of that money falls to about €47,600. So even though their €50,000 capital amount will still be on deposit, they will have lost about €2,400 in buying power.

After 5 years, the buying power falls to about €39,000 which means they have lost €11,000 buying power. After 10 years, that buying power falls to about €30,600.

Although inflation today exceeds 5%, it is expected that over time, it will fall back to more sustainable levels. The goal of the European Central Bank is to get it back to its target rate of about 2%. However, even at 2%, inflation can still have a very big impact.

Using the same €50,000 example, over a 10-year period, just 2% inflation will still reduce the buying power of that money to about €41,000. So, it still means that savers are still losing value, even though the capital amount on deposit remains the same (and is still protected under the Deposit Guarantee Scheme).

One means of countering the impact of inflation is to invest rather than leave too much sit on deposit or in a current account. In the current environment, this should be done cautiously.

Comments are closed.